PCB market is nearly 100 billion US dollars, and there is a broad space for domestic investment in packaging substrates and high-end HDI fields

Overall: Nearly 100 billion US dollars market, domestic investment in packaging substrates and high-end HDI fields has broad space

Market size: Macroeconomic recovery and emerging applications drive growth, and the global PCB output value is expected to exceed 5% CAGR from 2022 to 2026. PCB is called the “mother of electronic products” and is used in almost all electronic products, which is strongly related to the macro economy.

Affected by macroeconomic fluctuations, Prismark expects its output value to reach 82.1 billion US dollars in 2022, a year-on-year increase of 1.5%. Looking ahead, with the marginal weakening of macroeconomic influences, the overall demand has steadily recovered, and the emerging applications of servers and data centers, automotive electronics, AIoT (smart headphones, smart watches, AR/VR, etc.) have been released and technology has been upgraded. The output value of PCB is expected to grow steadily.

Prismark expects the global output value to reach 101.6 billion US dollars in 2026, and the CAGR from 2022 to 2026 will exceed 5%. From the downstream perspective: Smartphones account for the highest proportion, while servers and data centers, and automotive electronics have the fastest growth. According to Prismark data, smartphones, personal computers, consumer electronics, automotive electronics, servers, and data centers are the core application scenarios in the downstream of PCBs, and the output value is expected to account for 20%/16%/14%/11%/11% in 2022. In terms of growth rate, servers and data centers, and automotive electronics have the fastest growth, and the CAGR is expected to reach 9.4%/8.1% from 2022 to 2026.

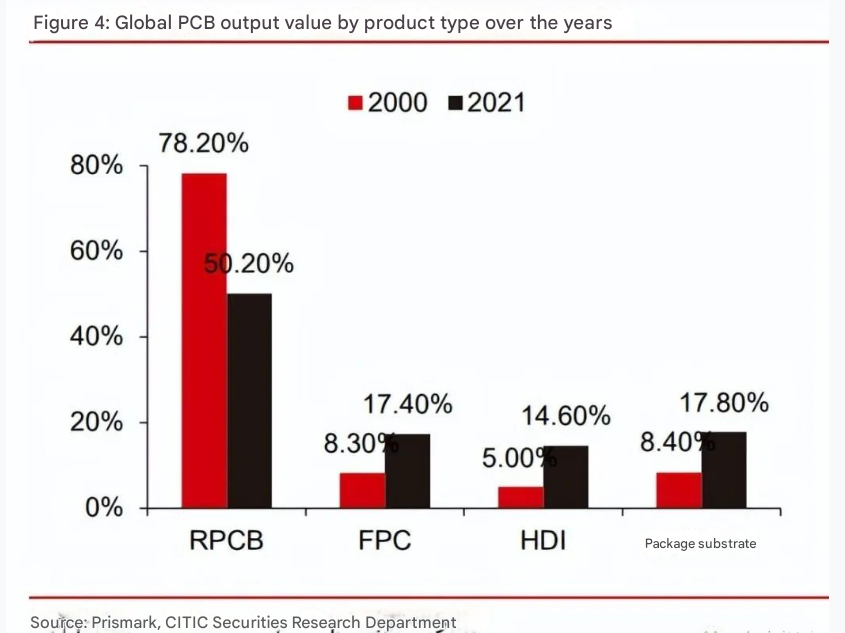

From the perspective of type: Technological development continues to promote the upgrading of PCB product structure, and the growth rate of packaging substrates and HDI boards is higher than the overall growth rate. Benefiting from the continuous iteration and upgrading of downstream application technical specifications, the requirements for circuit boards are also constantly improving, and the output value of mid-to-high-end products such as HDI and packaging substrates in the downstream of PCBs has increased significantly.

According to Prismark data, in 2000, RPCB (rigid circuit board)/FPC (flexible circuit board)/HDI (high-density interconnect board)/package substrate accounted for 78%/8%/5%/8% of the global PCB output value, and changed to 50%/17%/15%/18% in 2021, -28/+9/+10/+10pcts respectively. We believe that with the continuous upgrading of product performance, the output value of high value-added products is expected to maintain rapid growth. Prismark predicts that the global PCB overall output value CAGR will be about 4.6% from 2021 to 2026, of which package substrates are expected to be as high as 8.3%; followed by HDI boards, about 4.9%.

Competitive Landscape

There are many participating manufacturers, and there is broad space for domestic manufacturers to develop high-end substrates and HDI.

——Overall: PCB has the characteristics of strong customer customization and large specification differences. There are nearly 3,000 PCB companies in the world, and the overall market is fragmented. According to data from N.T.Information Ltd, the total output value of the top 30 manufacturers in the global PCB industry in 2021 was US$55.438 billion, accounting for 69% of the total scale, of which Taiwan, China, mainland China, South Korea, Japan, and others were 11/7/6/4/2, and the status of domestic capital continued to improve.

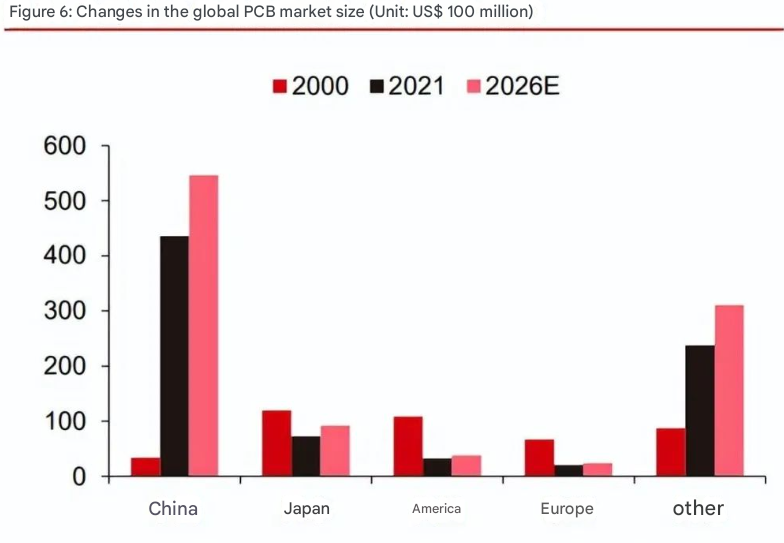

——From the perspective of regional distribution: According to Prismark data, with the rise of China’s manufacturing industry after 2000, the global PCB output value continued to shift from Japan, South Korea and Taiwan to mainland China. The mainland’s output value increased rapidly and its share in the world continued to increase, from US$3.4 billion in 2000 to US$43.6 billion in 2021, and the proportion increased from 8% to 55%, and it has become the core area of the global PCB industry.

From the perspective of different product specifications, the output value of the RPCB/HDI/package substrate market in mainland China is about 68%/63%/16% respectively, but HDI and package substrates are mainly produced by manufacturers in Taiwan, Japan, South Korea and other countries (such as Huatong, Xunda, Xinxing, Ibiden, Samsung Electro-Mechanics, etc.), and the proportion of domestic capital is still limited.

We believe that domestic manufacturers have basically dominated the RPCB field (high and multi-layers still need further breakthroughs). With the accumulation of R&D and technological upgrading, it is expected to gradually promote the high-end of products. It is expected to achieve rapid growth in the HDI and package substrate fields, and there is broad room for growth.