The high degree of customization of PCB is the most important feature of PCB.

There are very large differences in the scenarios, products, performance, materials, area, etc. when PCB is used, which leads to very large changes in the types of components used, the thickness of connecting wires, and the wiring density of different PCBs. Therefore, the degree of differentiation of different PCBs is very high. Generally, there are no two identical PCBs, which requires PCB companies to have very strong customized production capabilities. Although the PCB industry has some common basic processes, the most important thing is to determine different production processes and equipment according to the thickness and material of the substrate, the precision requirements of line width and line spacing, the design structure and production scale, and other special requirements specified by the customer.

Because the PCB industry has very strong customization characteristics, it is costly for customers to change PCB suppliers, so customers are usually willing to keep prices stable in order to obtain a stable supply of PCBs, so the price elasticity of PCB products is not large.

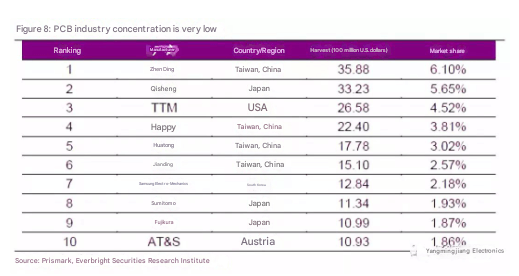

In addition, the customization characteristics of PCBs cause the efficiency of PCB manufacturers to usually decline as the scale expands, so the PCB industry is an industry with many participants and a very fragmented industry competition pattern. According to Prismark’s statistics, the world’s largest PCB manufacturer in 2017 was Zhen Ding in the *** region, with revenue of US$3.588 billion in 2017, and a market share of only 6.10% in the global PCB industry, while the market share of the top ten PCB manufacturers was only 33.51%, and the supply structure was very fragmented.

The characteristics of the production process determine that the profitability of the PCB industry does not rely on the technical level, but on the cost control ability.

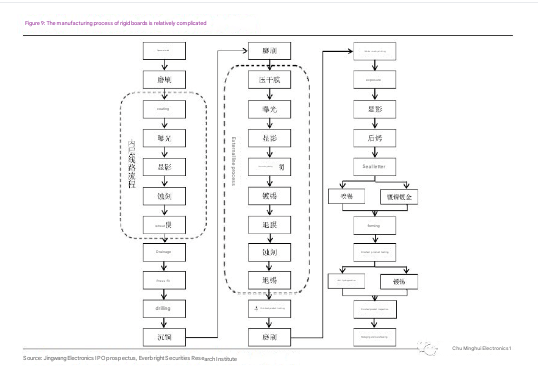

The production process of PCB is relatively complicated, usually with more than 40 processes such as inner layer production, blackening, lamination, drilling, and electroplating. Taking rigid circuit boards as an example, they usually include exposure, development, etching, copper plating, and film stripping. Although PCB has a strong customization feature, these most basic processes are necessary, but there will be differences in specific parameters.

Although the process is complicated, in fact, each process of PCB is not too difficult, and they are all relatively mature processes, and it is difficult for manufacturers to continue to make very large innovations in these processes. So in general, the technical differences between PCB companies are not large, and it is difficult to obtain higher profits through differences in technical levels.

Cost control ability directly determines the profitability of the company. We can see from the gross profit margins of key PCB companies in 2017 that Chongda Technology and Jingwang Electronics, as companies recognized by the industry as having strong cost control capabilities, also have relatively leading profitability in the industry.

Since the technical differences are not large, cost control ability has become the most critical factor in the profitability differences of PCB companies. Cost control is reflected in all aspects of the company’s operations and directly depends on the company’s management level. It needs to start from the details. For example, the “seven wastes” proposed by Jingwang Electronics are a reflection of the company’s management capabilities.

In the cost structure of PCB, direct material costs usually account for about 60%, direct labor costs usually account for about 15%, and manufacturing cost costs usually account for about 25%. However, copper clad laminate companies have a strong voice in direct costs, so PCB companies’ cost reduction is mainly achieved by reducing manufacturing and labor costs. Among them, reducing manufacturing costs is mainly achieved by improving production efficiency and yield through automation, and reducing labor costs is mainly achieved by transferring to the central and western regions.

Since the technical differences are not large, cost control ability has become the most critical factor in the profitability differences of PCB companies. Cost control is reflected in all aspects of the company’s operations and directly depends on the company’s management level. It needs to start from the details. For example, the “seven wastes” proposed by Jingwang Electronics are a reflection of the company’s management capabilities.